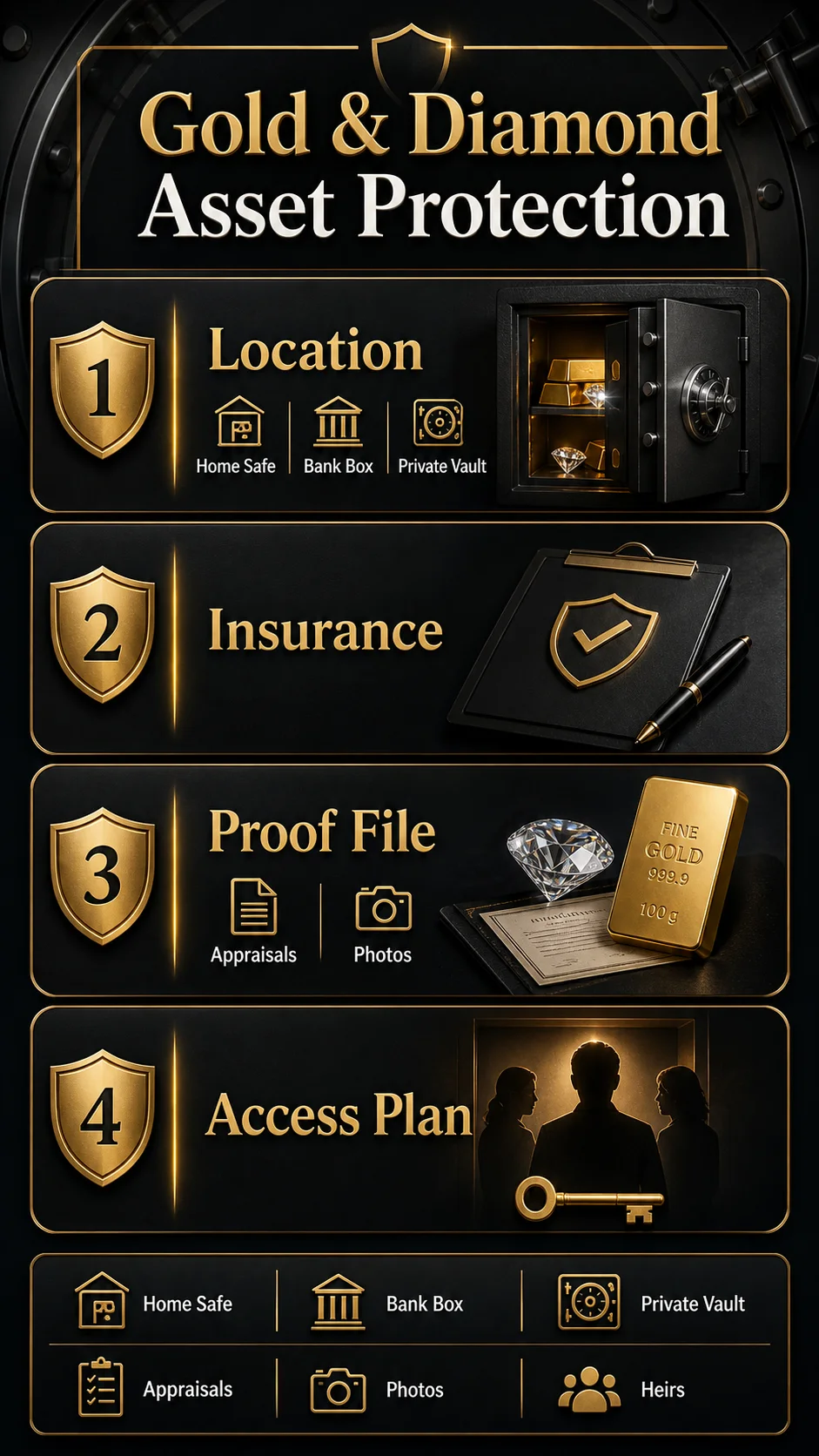

Compare home safes, bank boxes, insured vaults, and private storage for gold and diamonds, with documentation, insurance, access, and risk tradeoffs.

- Gold and diamonds need storage plus documentation, not just a safe location.

- Insurance depends on appraisals, proof files, policy limits, and custody records.

- Higher-value assets usually justify bank, vault, or private storage comparison.

Gold and diamond assets should be kept in a storage system, not just a hiding place. The safest setup combines the right location, written insurance, proof of ownership, and a clear access plan for the people who may need to recover the assets later.

That distinction matters because gold, diamonds, and jewelry fail in different ways. Bullion can be stolen or disputed. Diamonds can be hard to identify without grading reports and photos. Jewelry may be worn, inherited, damaged, or underinsured without the owner realizing it.

TL;DR

- For frequently worn jewelry: use a discreet home safe, updated appraisals, and scheduled insurance coverage.

- For rarely used heirlooms: a bank safe deposit box can make sense, but it is not automatically insured and can create access problems.

- For larger bullion or high-value collections: compare private vaults or specialized valuables storage with clear insurance and inventory rules.

- For diamonds: keep grading reports, appraisals, high-quality photos, and setting details outside the storage location.

- For families: create an access plan so heirs know where records are, who can access the assets, and what legal steps apply.

Short Answer: Where Should Gold and Diamond Assets Be Kept?

Small amounts of jewelry that you wear regularly can be kept at home if the safe is serious, the location is discreet, and the insurance is written for the actual value of the items.

Rarely used diamond jewelry, heirlooms, and important documents may fit a bank safe deposit box, especially if you do not need immediate access. The catch is that safe deposit box contents are not automatically covered by bank deposit insurance.

Larger bullion holdings or high-value collections often deserve private vault storage, allocated custody, or specialized valuables storage. The right choice depends on access, insurance, ownership records, jurisdiction, and how quickly the assets may need to be retrieved.

Gold vs Diamonds: Different Storage Problems

Gold and diamonds are both compact stores of value, but they are not documented in the same way.

This is why a simple “put valuables in a safe” answer is incomplete. Storage protects the item. Documentation protects your ability to prove and recover value.

Storage Options Compared

The best storage option depends on whether the asset is worn, held as bullion, kept as an heirloom, or stored as part of a broader estate plan.

| Storage option | Best fit | Main advantage | Main risk | Proof and insurance question |

|---|---|---|---|---|

| Home safe | Frequently used jewelry, small gold reserve, documents needed quickly | Immediate access and privacy | Theft, fire, disclosure, and household concentration risk | Does your policy cover the items at home, and are they scheduled? |

| Bank safe deposit box | Rarely used valuables, heirlooms, backup documents | Better physical security than most homes | Limited access, lease restrictions, estate friction, no automatic deposit insurance | Does off-premises valuables coverage apply to box contents? |

| Private vault | Larger bullion, high-value jewelry, long-term custody | Professional security, inventory process, possible insurance clarity | Fees, provider diligence, jurisdiction, withdrawal rules | Are the assets inventoried, insured, and recoverable under written terms? |

| Allocated bullion storage | Physical gold ownership where specific bars or coins should be assigned | Stronger ownership quality than a general claim | Costs more and still depends on contract language | Can specific metal be matched to you? |

| Split storage | Mixed assets with different access needs | Reduces one-location failure risk | More documentation and administration | Can your records explain where each asset is and why? |

Home Safe: Best for Access, Not for Everything

A home safe is practical for jewelry you wear, emergency documents, and a small amount of gold you may want to access without waiting on a bank or custodian.

The risk is that home storage can become too convenient. If the value grows and everything remains in one place, a single burglary, fire, or disclosure can create a major loss.

Home storage works best when:

- The safe is properly rated, installed, and difficult to remove.

- The valuables are not casually discussed with friends, contractors, or extended family.

- Insurance coverage is confirmed in writing.

- Appraisals and photos are stored somewhere other than the safe.

- Only a limited portion of the total valuable assets are kept at home.

For gold-specific home storage tradeoffs, see GoldConsul’s guide to home safe vs private vault for gold.

Safe Deposit Box: Strong Physical Security, Weak Assumptions

A safe deposit box can be useful for heirloom jewelry, diamond paperwork, coin records, and valuables that do not need daily access.

But a bank box is not the same as a bank deposit. FDIC deposit insurance does not cover gold, diamonds, jewelry, cash, or documents stored inside a safe deposit box.

Access can also be a real issue. If the owner dies, becomes incapacitated, loses the key, misses rental payments, or fails to name an authorized person, family members may face delays even if they know the box exists.

For the gold-specific insurance boundary, read GoldConsul’s article on whether gold is insured in a safe deposit box.

Private Vault or Specialized Valuables Storage

Private vaulting becomes more relevant when the asset value is high enough that one household location feels too exposed.

For bullion, that may mean allocated storage with bar records. For diamonds and jewelry, it may mean a specialized storage provider, insurer-approved storage, or a vault arrangement with documented inventory and access procedures.

Compare professional storage by:

- Insurance scope, exclusions, and deductibles.

- Inventory records and whether assets are individually identified.

- Access rules for owners, authorized persons, and estates.

- Audit practices and provider reputation.

- Jurisdiction, fees, withdrawal process, and shipping options.

If your main concern is physical bullion rather than jewelry, the broader GoldConsul hub on where to store gold compares home safes, bank boxes, private vaults, allocated storage, and split storage in more detail.

The Proof File: The Layer Most People Miss

A proof file is the set of records that shows what existed, what it was worth, where it was kept, and who had rights to access it.

Without a proof file, insurance claims and estate administration become harder. The asset may be real, but the burden of proof may fall on the owner or heirs.

For gold, keep:

- Purchase invoices and dealer confirmations.

- Weight, purity, refiner or mint details.

- Bar numbers, certificate numbers, or packaging details where applicable.

- Photos or video of coins, bars, and packaging.

- Storage contracts and insurance documents.

For diamonds and jewelry, keep:

- Grading reports for significant diamonds.

- Appraisals with replacement values and item descriptions.

- Photos from multiple angles, including hallmarks and settings.

- Receipts, repair records, resizing records, and provenance notes.

- Insurance schedules and any coverage endorsements.

Insurance Checklist

Insurance is where many storage plans break. A homeowner or renter policy may not fully cover jewelry, bullion, collectibles, or off-premises valuables unless the items are scheduled or specifically endorsed.

Ask your insurer these questions:

- Are gold bullion, coins, diamonds, and jewelry covered at replacement value or only up to a sublimit?

- Does coverage apply at home, in a safe deposit box, in transit, and in a private vault?

- Which items need appraisals or grading reports?

- How often should appraisals be updated?

- Are mysterious disappearance, theft, fire, flood, and accidental damage treated differently?

- Are there exclusions for business inventory, investment metals, or unscheduled valuables?

For jewelry specifically, major insurers often recommend current appraisals, diamond certificates where relevant, and clear documentation. That advice is not paperwork clutter; it is claim preparation.

Split Storage Plan for Gold and Diamond Assets

Split storage is often the most resilient system for mixed valuables. It avoids treating every asset as if it has the same access need and the same risk profile.

For bullion investors, this can pair with the difference between allocated and unallocated gold storage. If the gold is meant to be physically owned, the storage contract should support that goal.

Estate Access: The Awkward Problem to Solve Early

Valuables often create problems after the owner is gone because nobody knows what exists, where it is, how to access it, or whether insurance still applies.

You do not need to share every detail with everyone. But at least one trusted person, executor, or adviser should know where the records are and what steps are required.

Estate access checklist:

- List storage locations without publishing them broadly.

- Document who is authorized to access each location.

- Keep safe deposit box details and keys handled according to legal advice.

- Store appraisals, photos, and insurance documents where heirs can find them.

- Update records after sales, gifts, repairs, inheritance, or storage changes.

The GoldConsul Editorial Perspective

Secure storage is a system: location, proof, insurance, and access. A vault can protect the object, but only records and planning protect your ability to prove ownership, recover value, and pass assets on cleanly.

Knowledge Gap: The Real Risk Is Not Only Theft

Most valuables-storage advice focuses on where to hide or store the item. That is only one part of the problem.

- Theft risk: can someone take it?

- Proof risk: can you prove what was taken?

- Coverage risk: will insurance respond?

- Access risk: can the right person retrieve it when needed?

- Ownership risk: is the asset clearly yours or clearly assigned to your estate?

The strongest plan reduces all five risks instead of treating a safe as the whole solution.

Helpful Starting Points

If you are still building your broader precious-metals plan, start with GoldConsul’s free gold guide for beginners. It covers coins, bars, premiums, storage, and resale basics.

For external background, review the FDIC deposit insurance FAQ for what bank deposit insurance does and does not cover. A major bank’s safe deposit box explainer, such as Chase’s safe deposit box guide, is also useful for understanding access and usage basics. For jewelry, Chubb’s jewelry-protection guidance highlights why appraisals, certificates, and documentation matter.

FAQ: Where Should Gold and Diamond Assets Be Kept?

Should gold and diamonds be kept at home?

Small or frequently used items can be kept at home if the safe is properly installed, the location is discreet, and the insurance is written for the actual value. Larger holdings usually deserve split storage or professional storage.

Are diamonds safe in a bank safe deposit box?

A bank box can improve physical security, but it does not automatically provide insurance or easy estate access. Keep grading reports, appraisals, and photos outside the box as part of a separate proof file.

Does insurance cover gold and diamond jewelry?

It depends on the policy. Many policies have sublimits or exclusions for jewelry, bullion, collectibles, or off-premises valuables unless items are scheduled or endorsed separately.

What documents should I keep for diamonds?

Keep grading reports, appraisals, receipts, photos, setting details, repair records, and insurance schedules. Store copies separately from the diamond itself.

Should heirs know where gold and diamond assets are stored?

At least one trusted person, executor, or adviser should know where the records are and how access works. You can protect privacy while still leaving a usable recovery path.

Bottom Line

Gold and diamond assets should be kept where the storage method matches the asset type, value, usage pattern, insurance position, and access needs.

A home safe may fit daily jewelry and small reserves. A safe deposit box may fit rarely used heirlooms and documents. A private vault or specialized storage provider may fit larger collections. The strongest plan combines storage with proof, insurance, and estate access.

When you purchase a service or a product through our links, we sometimes earn a commission, at no extra cost to you.

When you purchase a service or a product through our links, we sometimes earn a commission, at no extra cost to you.