Gold can diversify recession risk but may fall in a cash scramble. Compare real yields, dollar, liquidity, costs, drawdowns, and portfolio role.

- A safe haven is defined relative to a specific risk and time window; gold does not rise in every recession or every crash week.

- Gold often benefits when real yields fall, the dollar weakens or confidence risk rises, but cash demands can trigger temporary selling.

- Use a target allocation, liquidity reserve, total-cost comparison and rebalancing rule instead of buying only after fear spikes.

- A hedge, safe haven and diversifier are different claims.

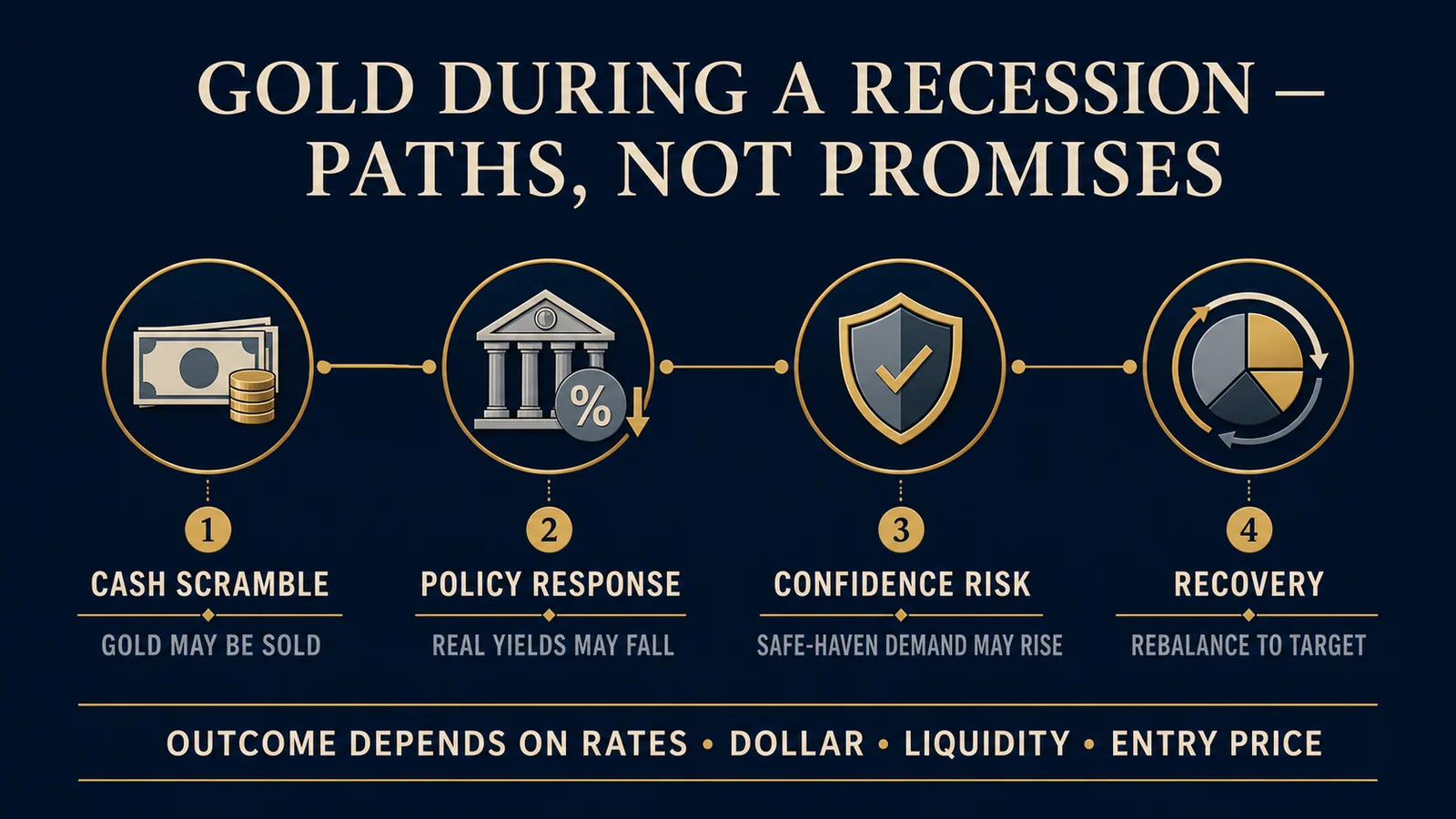

- Gold may fall early in a liquidity shock as investors raise cash.

- Lower real yields and confidence stress can later support demand.

- Physical gold, ETFs and gold-mining stocks carry different risks.

- Allocation size, costs and rebalancing determine the portfolio outcome.

A conditional defense, not an automatic recession trade

The most useful question is not “Does gold rise in recessions?” It is “What risk am I trying to offset, through which instrument, over what horizon?” A short NBER recession window, a stock-market drawdown and a multi-year inflation shock can overlap, but they are not the same event.

Hedge, safe haven and diversifier

| Term | Practical meaning | Evidence needed |

|---|---|---|

| Hedge | Tends to offset another asset or risk on average. | Relationship across ordinary periods. |

| Safe haven | Holds value or offsets losses during specified stress windows. | Performance in tails, with the window defined. |

| Diversifier | Does not move exactly with the rest of the portfolio. | Correlation and contribution to total portfolio risk. |

Baur and Lucey’s academic work formalized the hedge/safe-haven distinction. A haven relationship can be temporary and market-specific; a low long-run correlation does not promise a gain on the worst day.

Why gold may fall first in a recession shock

During a sudden liquidity crisis, investors may sell assets that have a ready market—including gold—to meet margin calls, redemptions or cash needs. The dollar may strengthen, and real yields may move unexpectedly. A temporary gold decline therefore does not disprove every safe-haven property; it shows that timing and funding stress matter.

Later, aggressive policy easing, falling real yields, banking stress, fiscal concerns or loss of confidence can make a non-yielding monetary asset more attractive. The path in the infographic is a scenario sequence, not a forecast.

The main drivers to monitor

| Driver | Potential support for gold | Potential headwind |

|---|---|---|

| Real yields | Falling inflation-adjusted yields reduce opportunity cost. | High or rising real yields increase the attraction of bonds and cash. |

| U.S. dollar | A weaker dollar can support dollar-denominated gold. | A cash scramble can strengthen the dollar. |

| Financial confidence | Banking or sovereign concern can increase haven demand. | Stable confidence can reduce urgency. |

| Official demand | Central-bank diversification can create structural buying. | Purchases can slow and are not a daily price guarantee. |

| Positioning and flows | ETF inflows and futures demand can amplify gains. | Liquidation can amplify losses. |

Track the mechanism rather than a headline. FRED’s 10-year real-yield series, gold benchmark data and broad dollar measures can be aligned by date, but correlation is not proof of a single cause. See the deeper gold price factors framework.

Different recession types can produce different gold paths

The NBER dates U.S. business-cycle peaks and troughs retrospectively. An investor usually does not receive the official recession label at the market turning point.

How to test the safe-haven claim with history

Start with a predeclared window and currency. Compare gold with the asset or liability it is supposed to protect, then include transaction costs. Test the first drawdown phase separately from the full recession and recovery. A result in U.S. dollars may differ for an investor whose spending and taxes are in euros or yen.

FRED’s historical London gold fixing series can be aligned with recession dates and market data. Beware of daily observations that use different market-close times. The question is portfolio contribution, not whether one cherry-picked endpoint is positive.

- Record the business-cycle or market-stress dates before seeing the answer.

- Measure gold in the investor’s base currency.

- Separate peak-to-trough, full recession and 12-month follow-through.

- Compare physical or fund costs with the selected benchmark.

- Repeat across several episodes and report failures.

Gold instrument choice changes the risk

| Exposure | Strength | Extra risk or cost |

|---|---|---|

| Physical coins/bars | Direct possession outside a brokerage | Dealer spread, storage, insurance and authentication |

| Physically backed ETF/trust | Liquidity and easy rebalancing | Fee, tracking, market price and custody structure |

| Gold-mining shares | Business leverage to the gold industry | Operating, equity, jurisdiction and management risk |

| Futures/leveraged products | Capital efficiency or tactical exposure | Leverage, roll, margin and path risk |

Read how gold ETFs work before assuming a security equals a bar, and compare the broader routes in how to invest in gold. Gold miners are equities; they can fall with the stock market even while bullion is resilient.

A worked core-allocation example

A $100,000 portfolio sets a 5% gold target, or $5,000, with a policy band of 3%–7%. If the rest of the portfolio falls and gold rises until gold becomes 7.4% of the new total, the rule calls for trimming toward target. If gold falls to 2.8%, the rule calls for reviewing assumptions and, if still valid, buying toward target.

This is an arithmetic illustration, not a recommended allocation. Taxes, account type, spread and personal liquidity needs can change the sensible action.

Why entry price and holding period matter

An asset can serve a long-horizon diversification role and still be a poor short-horizon purchase after a crowded rally. The relevant return begins on the investor’s purchase date, not at a conveniently chosen recession start. Compare total cost and define what would trigger a sale or rebalance before volatility arrives.

The World Gold Council’s mid-year 2026 outlook describes a high-volatility environment and scenario drivers. It is an industry source, not an independent forecast, and should be read alongside market data and the current policy backdrop. Do not translate “safe haven” into a hardcoded live-price claim.

Gold versus other defensive assets

Cash provides known nominal liquidity but loses purchasing power when inflation exceeds its yield. High-quality sovereign bonds can produce income and often help in disinflationary recessions, though duration suffers when rates rise. Gold has no contractual yield or defaulting issuer, yet it has price risk and ownership costs. The instruments solve different problems.

Real estate is illiquid and locally financed; compare it carefully in gold versus real estate in a recession. Crypto has a different liquidity and drawdown record; see gold versus crypto.

Currency and storage are part of the outcome

Gold is commonly quoted in dollars, but a non-U.S. investor experiences both the metal move and exchange-rate move. A rising local-currency gold price can reflect weaker local money rather than a higher dollar gold price. Hedged and unhedged securities may therefore behave differently.

Physical ownership also requires a recovery plan: secure storage, insurance terms, access during disruption and a documented resale route. Review where to store gold. A haven that cannot be accessed, authenticated or sold at a reasonable spread may fail the practical objective even if the benchmark price rises.

For exchange-traded exposure, check the prospectus, custody arrangement, trading spread and tax treatment before a crisis. Operational due diligence done during calm markets is part of safe-haven planning; product labels alone do not establish resilience.

Review the plan after major changes in income, liabilities or portfolio concentration. A static percentage chosen years earlier may no longer address the risk that originally justified it.

The rule should remain understandable to the person who must execute it during stress.

Due-diligence checklist before buying “for the recession”

- Name the risk: equity loss, inflation, banking access, currency or general uncertainty.

- Set the maximum portfolio weight and rebalancing band.

- Choose physical, ETF or another instrument for a stated reason.

- Calculate spread, annual fees, storage and tax effects.

- Keep emergency cash separate; do not rely on a volatile asset for next month’s bills.

- Use limit orders and reputable dealers or brokers.

- Define review dates and conditions that would invalidate the thesis.

Failure modes to avoid

- Binary thinking: expecting gold to rise on every negative economic release.

- Instrument confusion: treating miners, leveraged ETFs and physical bars as the same exposure.

- Price anchoring: citing a past crisis without matching entry and exit dates.

- Liquidity mismatch: spending emergency cash on high-premium products.

- No exit rule: buying from fear and deciding later what the holding is for.

Many safe-haven charts select one recession, one currency and one endpoint. A serious evaluation shows the initial cash scramble, policy response, instrument costs and portfolio-level result. It also reports counterexamples rather than using only episodes that flatter gold.

Gold is most defensible as insurance with a budget. Insurance is not expected to “win” every year; it is sized so its cost and volatility do not endanger the plan. The safe-haven label should narrow a role, not suspend valuation or risk controls.

This article is educational and not personalized investment, tax or legal advice. Gold can lose value, and historical stress performance does not guarantee future results. Consider your jurisdiction, time horizon and ability to bear loss.

Selected explainer This video adds a concise visual explanation to the evidence and decision framework above.

Bottom Line

Gold can help during some recessions, especially when real yields fall or confidence in financial claims weakens, but it may be sold during the first liquidity shock. Define the risk, choose the right instrument, limit the allocation, include all costs and rebalance by rule rather than fear.

FAQ: Gold as a Safe Haven During Recession

Does gold always go up in a recession?

No. It can fall during cash scrambles, strong-dollar periods or rising real yields. Results depend on the recession type and time window.

Is physical gold safer than a gold ETF?

Physical removes some brokerage dependence but adds storage, insurance and transaction costs. An ETF adds fund and custody structure but is easier to trade and rebalance.

Are gold-mining stocks a safe haven?

They are operating companies and equities, so they add business and stock-market risk. Their performance can differ sharply from bullion.

How much gold should I own before a recession?

There is no universal percentage. A suitable allocation depends on purpose, liquidity, other assets, taxes and risk tolerance; use a capped policy rather than a fear-driven purchase.

What indicators matter most for gold in a downturn?

Real yields, the U.S. dollar, liquidity stress, policy response, official demand, ETF/futures flows and confidence are more informative than the recession label alone.

Sources and verification

Values, rules and historical interpretations were checked against the linked primary or specialist sources. Recheck any current rule or market data before acting.

- World Gold Council — Mid-Year Outlook 2026 — Current scenarios for growth, rates, dollar, risk and gold; industry source.

- World Gold Council — Strategic Asset 2026 — Liquidity, diversification, returns and risk framework; industry source.

- IMF — Gold as International Reserves — Safe-haven and reserve-diversification evidence in official holdings.

- NBER — Business Cycle Dates — Authoritative U.S. recession dates for historical comparisons.

- FRED — Gold Fixing Price — Daily London gold price series for time-window analysis.

- FRED — S&P 500 — Equity benchmark series for defined drawdown comparisons.

- FRED — 10-Year Real Yield — Inflation-indexed Treasury yield proxy for gold opportunity cost.

- Investor.gov — Diversification — Regulator guidance on asset allocation and diversification.

- Baur and Lucey — Is Gold a Hedge or Safe Haven? — Academic distinction between hedge and safe-haven behavior.

- CNA — Why Is Gold a Safe Haven Asset? — Accessible visual overview of gold’s safe-haven role and limits.

When you purchase a service or a product through our links, we sometimes earn a commission, at no extra cost to you.

When you purchase a service or a product through our links, we sometimes earn a commission, at no extra cost to you.